In May, we released an in-depth look at the experiences of small business owners across Texas in the first month of the crisis. In the subsequent months, there have been updates to existing resources, and more initiatives have launched to support small firms across the country and state.

The $349 billion initial rollouts of Paycheck Protection Program (PPP) funding in early April suffered some technical glitches and concerns regarding the types of firms reaping the benefits.

Given that banks are typically required to undertake a firm vetting process when making loans but faced a tight timeline for disbursing PPP funds, a prior lending relationship appeared critical to receiving round one of PPP loans.

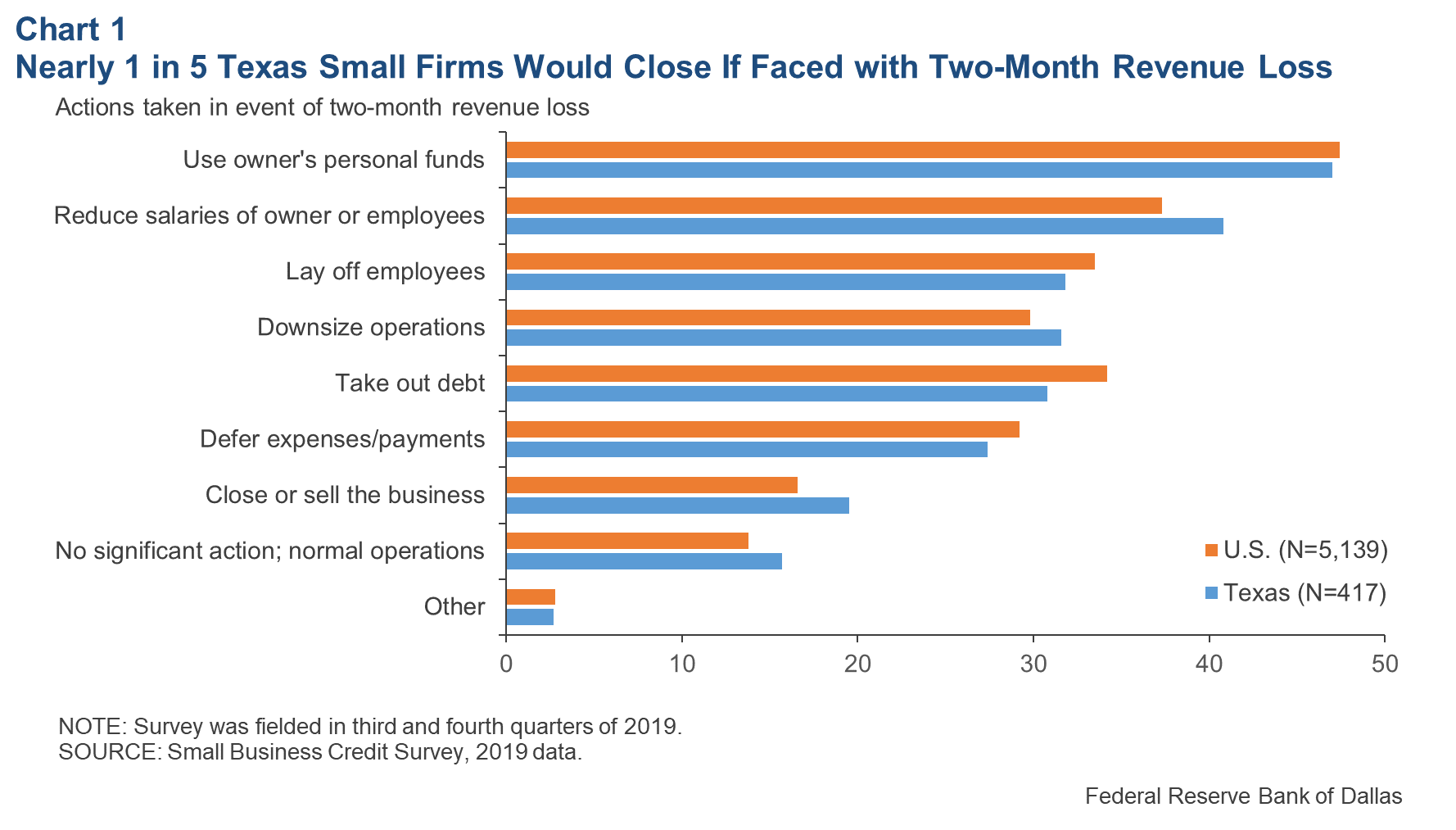

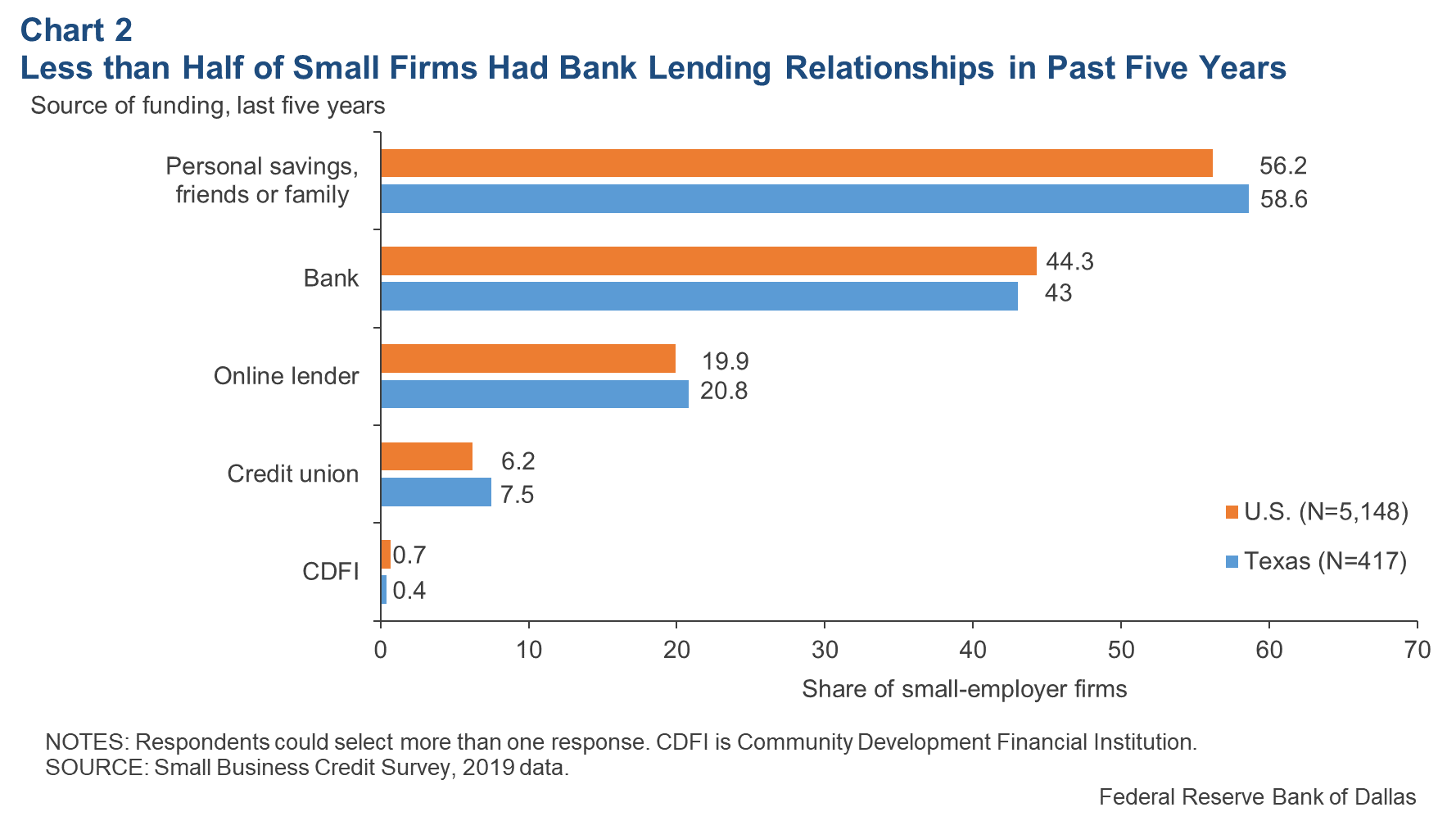

This matters because prior bank lending relationships (beyond a traditional savings or checking account) are less prevalent for many small firms than one might expect—particularly among certain subsets like minority-owned businesses or microfirms.

According to 2019 data from the Fed’s Small Business Credit Survey, just 44 percent of small-employer firms in the U.S. used a bank lender within the prior five years. At 43 percent, the Texas share was slightly smaller (Chart 2). Firms that did have such a bank relationship tended to be larger and were more likely to be white-owned.

Recognizing the need for both additional funds and a more-inclusive process, Congress passed an extra $310 billion in second-round PPP funding, including:

Granular data are necessary to understand how well this second, more-targeted round of funding has reached all communities. Taking a significant step toward this goal, on July 6, the Small Business Administration (SBA) and the Treasury Department released loan-level data on the 4.9 million PPP loans made thus far.

According to early analysis, Texas issued the second-largest aggregate loan amount, which at $41.1 billion, is only surpassed by California’s $68.2 billion. However, as a share of small business payroll, Texas falls squarely in the middle of the 50 states.

PPP funds went to firms representing about 82 percent of small business payrolls in Texas—about halfway between Florida’s and Hawaii’s 96 percent and Virginia’s 72 percent.

There are businesses in approximately 157 cities in Texas listed as receiving some amount of PPP funds.

Determining the reach of dollars to minority-owned and/or women-owned firms is much more challenging, given the significant number of PPP recipients who did not disclose firm ownership demographics.

Finally, a few additional regulatory shifts took place in June, loosening restrictions for small business borrowers:

These first two changes retroactively apply to March 27, 2020, the date the Coronavirus Aid, Relief and Economic Security (CARES) Act was originally passed. The third change related to loan maturity only applies to loans made on or after June 5, 2020.

Beyond the PPP, other resources exist at the federal level. Two important updates since publishing our May 12 article on small businesses and COVID include:

Beyond resources at a national level, many cities across Texas have recognized the need for additional support in their small business communities. In Dallas, for instance, a multisector approach led to the development of the Revive Dallas Small Business Relief Fund.

Private businesses, the Communities Foundation of Texas (CFT), LiftFund, and the Dallas Entrepreneur Center Network all play a role in the fund. The fund specifically targets businesses in Dallas that employ a maximum of 15 employees and that have experienced at least a 15 percent loss of revenue since the onset of the COVID crisis.

A majority of loans are dedicated to women-owned or minority-owned firms. With 0 percent interest, they are fully forgivable if participants meet certain requirements, including participating in a mentorship program and creating a 2021 budget.

Sejal Desai, a business engagement director for CFT, the fund’s fiscal sponsor, notes the goal of the collaborative was to provide small businesses not solely with funding but also “wrap-around, full-service support.” She says, “Many businesses can use not only the money but also mentoring from business leaders who are successfully managing to pivot during these unprecedented and challenging times.” The Revive Dallas fund plans to total $5 million, nearly half of which has already been raised.

Various other local resources exist across the state. Some of these include:

A June 2020 Dallas Fed analysis highlights the particular challenges small businesses face, including the fact that in normal economic times, only about half of startups survive more than five years. Small firms tend to struggle more with credit access than larger firms, a phenomenon that is amplified in times of economic crisis.

In fact, the analysis points out that small businesses suffered greater job losses than larger ones during the two recessions of the 2000s, and small business lending fell during the Great Recession and stayed below prerecession levels.

It’s clear that small firms—and the overall economy—are once again facing a very significant challenge. What remains to be seen is how effective the historic federal economic relief packages will be at stemming the widespread revenue losses for small firms throughout the U.S. and Texas and how equal the recovery may be among communities.

Notes

Emily Ryder Perlmeter is a community development advisor at the Federal Reserve Bank of Dallas.

The San Marcos City Council received a presentation on the Sidewalk Maintenance and Gap Infill…

The San Marcos River Rollers have skated through obstacles after taking a two-year break during…

San Marcos Corridor News has been reporting on the incredible communities in the Hays County…

Visitors won't be able to swim in the crystal clear waters of the Jacobs Well Natural…

Looking to adopt or foster animals from the local shelter? Here are the San Marcos…

The Lone Star State leads the nation in labor-related accidents and especially workplace deaths and…

This website uses cookies.

{kind=link}

{kind=link}