Texas Facing Historically Tight Labor Markets, Constraining Growth

By Christopher Slijk

Texas labor markets have become exceptionally tight over the past year. Since the end of the oil bust of 2015–16, many measures of labor market slack have declined to multidecade lows. This trend has been largely uniform, affecting all of the state’s major regions as jobless rates have reached or surpassed previous record lows.

These trends coincide with similar labor constraints across the U.S.

A tight job market significantly affects the economy. It increases workers’ bargaining power and pushes up wages and benefits. It limits companies’ ability to expand because finding and retaining workers becomes more difficult even as labor costs increase.

When such labor scarcity becomes pervasive across industries, it can constrain economic growth and, over the longer term, may provide stronger incentive for businesses to boost investments in labor-saving technologies.1

Labor Force Migration, Growth

Since the Great Recession ended a decade ago, the Texas job market has experienced a robust recovery. Texas’ employment expansion preceded U.S. job growth, and by 2012, the state had exceeded its prerecession employment peak. Texas job growth from 2010 to 2018 outpaced its long-term trend of 2.1 percent on average. Over this time, Texas became the fourth-fastest-growing state, trailing only Nevada, Florida and Colorado, despite an oil bust in 2015–16.

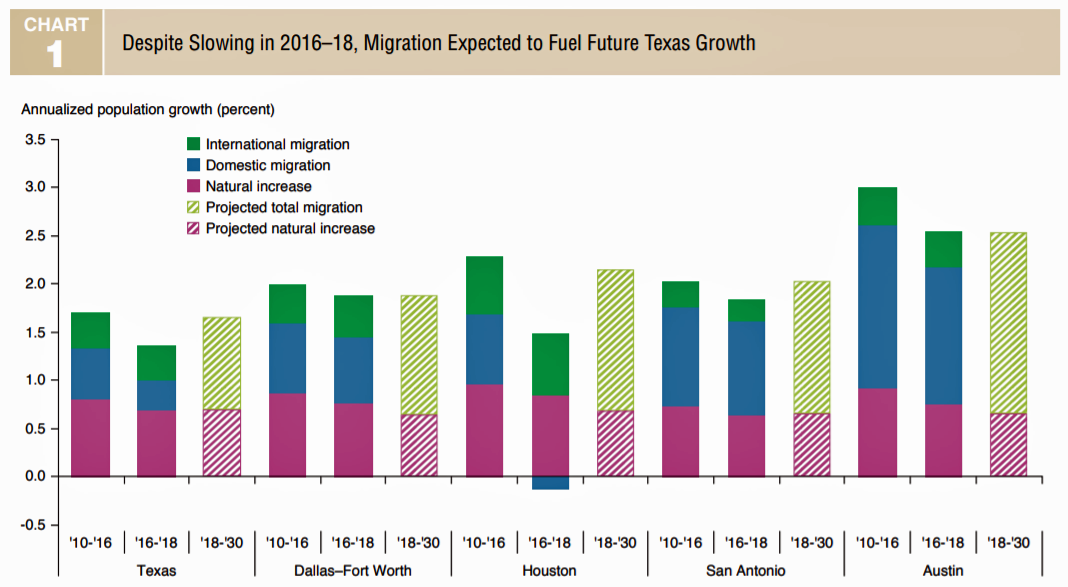

Meanwhile, data available covering 2010–17 show the working-age population (ages 16 to 64) grew just 1.5 percent per year. Migrants to the state augmented this growth. Domestic and international migration have accounted for nearly half of overall Texas population growth since 2010 and an even larger share of the growth of the working-age population, reflecting that many move to Texas for employment.2

Recent data suggest that these movements have slowed; since 2016, the share of population increase attributable to domestic migration has nearly halved, dropping average annual growth to just 1.3 percent over the past two years (Chart 1). Some of this deceleration is likely due to the U.S. economic expansion in recent years— as employment prospects improved and unemployment rates declined broadly across the nation, the need for job seekers to incur the costs of moving to Texas for work diminished.

The change in migration patterns has been most striking in Houston as the area flipped from being a top region for domestic migration in 2010–16 to experiencing a net outflow the following two years.

Data from the Texas Demographic Center suggest that through 2030, the majority of overall population growth in the state and its major metros will come from a combination of domestic and international migration.

Natural increase—the number of births relative to deaths—is expected to continue declining as a driver of population growth in Texas and the rest of the U.S.

This change is even starker among the working-age population—more than three-fourths of the 1.4 percent annual growth expected through 2030 is projected to come from net domestic and international migration. This will constitute a majority of labor force growth over the period.

Record Low Unemployment

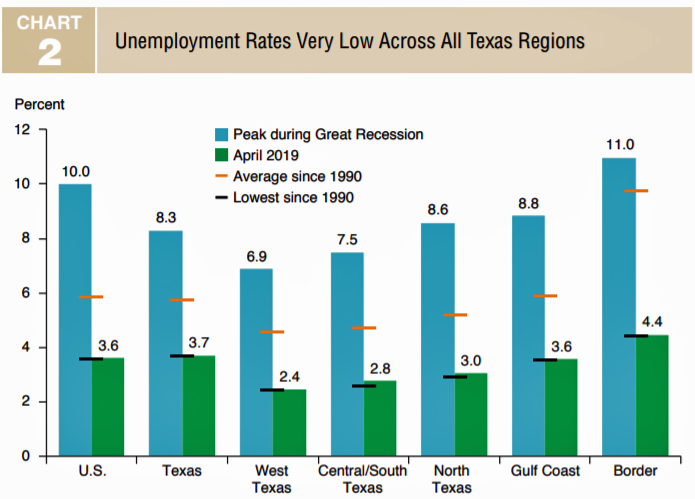

With the number of workers failing to keep up with the rapid increase in employment, labor availability has tightened in Texas. The state unemployment rate, after peaking at 8.3 percent in late 2009, has steadily declined. The rate stood at 3.7 percent in April 2019, its lowest level since records began in the mid-1970s. Texas’ unemployment rate of 4 percent or below for over a year suggests unprecedented labor market tightness.

Broader measures of labor market slack further illustrate the unusual level of constraint. The U.S. Bureau of Labor Statistics’ broader U-6 measure of state unemployment—which includes discouraged workers (who have given up looking for work in the last 12 months) and those who are working part-time but would like to work full-time— reached a record low of 7.2 percent in early 2019. This is significantly below the 25-year average of 9.9 percent and well below the recessionary peak of over 15 percent.

Looking more closely at regions within the state, a similar picture emerges. Jobless rates remain significantly below their long-term averages and are less than half of their Great Recession peaks (Chart 2). Among urban areas, only the Texas border region has a higher jobless rate than the U.S. and Texas.

Regional Areas of Strength

West Texas, which includes the energy-intense Permian Basin and Midland–Odessa, has the lowest unemployment rate in the state, 2.4 percent, and is one of the tightest labor markets in the nation. “Man camps” have sprung up around Midland–Odessa; housing shortages abound as workers rush into the region to fill lucrative jobs in the oil and gas industry.

Along the Interstate 35 corridor’s populous metropolitan areas, labor markets are constrained, though slightly above their all-time unemployment lows. The four largest metros—Dallas, Fort Worth, Austin and San Antonio—nationally rank in the top 25 of large metro areas (population of over 1 million) for lowest rates of joblessness.

Nevertheless, they continue experiencing strong labor force growth, with the North Texas region growing well above average at 2.3 percent, and the Central/South Texas labor force expanding at close to the state average of 1.5 percent year over year through April.

These regions benefit the most from migration to the state. The population age 25 to 64 is expected to grow about 2 percent annually through 2030 based on recent population trends—and most of that growth (1.9 percentage points) is projected to be from a mix of domestic and international in-migration.

The Gulf Coast region—dominated by metropolitan Houston—has record low unemployment after joblessness rose in the oil bust years of 2015–16. A net outmigration of people followed the slump, possibly exacerbated by Hurricane Harvey in August 2017. These departures, combined with the energy sector rebound in 2017–18, led to an unprecedented tightening of regional labor markets.

The Texas–Mexico border stands out as the one region with a significantly higher unemployment rate than the state average. Still, the 4.4 percent jobless rate in April was a record low for the region. Its young, predominantly Hispanic population has historically grown faster than the state and national averages.

However, recent slowing in the pace of labor expansion—down to just 0.4 percent year over year—has pushed the jobless rate to less than half of its long-term average. Proximity to high-paying oilfield jobs in the Eagle Ford and Permian Basin shale plays, along with declining appeal as a final destination for Mexican immigration, may factor into this slowing. The region overall has experienced net outmigration since 2013.

Struggling to Hire

Recruiting and retaining hires has become increasingly difficult for Texas businesses. Starting in late 2017, a majority of surveyed firms have had difficulties finding qualified applicants to fill open positions, the Federal Reserve Bank of Dallas’ Texas Business Outlook Surveys (TBOS) show.

Comments from businesses have persistently pointed to the lack of workers impeding company expansion and slowing hiring.

“We simply cannot find enough legal entry-level workers to complete our work. We are actively turning away new business. Despite all efforts including pay increases, hiring and referral bonuses, etc., we are unable to keep a full staff,” a survey respondent in professional and business services noted in April. “We will ultimately lose close to $2 million in revenue this year due to lack of available labor.”

Other survey contacts have mentioned similar constraints, with one financial services firm saying that the “lack of a qualified workforce is our leading contributor to stalled growth.”

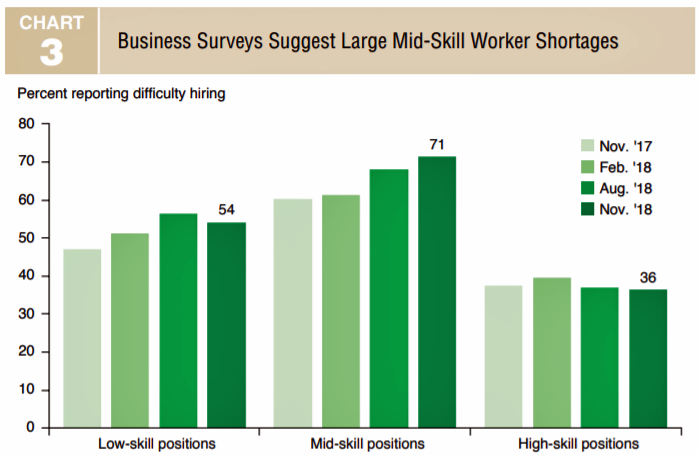

While labor tightness is broad based, it has been particularly acute for firms seeking to fill mid-skill positions—those requiring some college or technical training (Chart 3). The positions include many blue-collar trades, which respondents have identified as constrained nationally for the past several years.3

TBOS surveys have noted increasing difficulty finding mid-skill workers, with nearly threequarters of hiring firms saying they struggled to recruit for such positions in November 2018.

Texas Employer Impact

Responding to this persistent inability to find workers, businesses have looked to a number of alternative strategies to attract labor. Intensified recruiting—the predominant method until mid-2018—included more advertising, greater utilization of employment agencies and sign-on bonuses.

More recently, employers have turned to increasing wages and benefits as the primary means of dealing with the labor shortage. The share of TBOS respondents reporting that they had resorted to such increases has risen sharply, from about 50 percent in early 2018 to 67 percent by yearend.4

As one contact in the hospitality industry noted in March 2019, “Hiring remains a huge problem, so we anticipate increases in wages and benefits just to compete.”

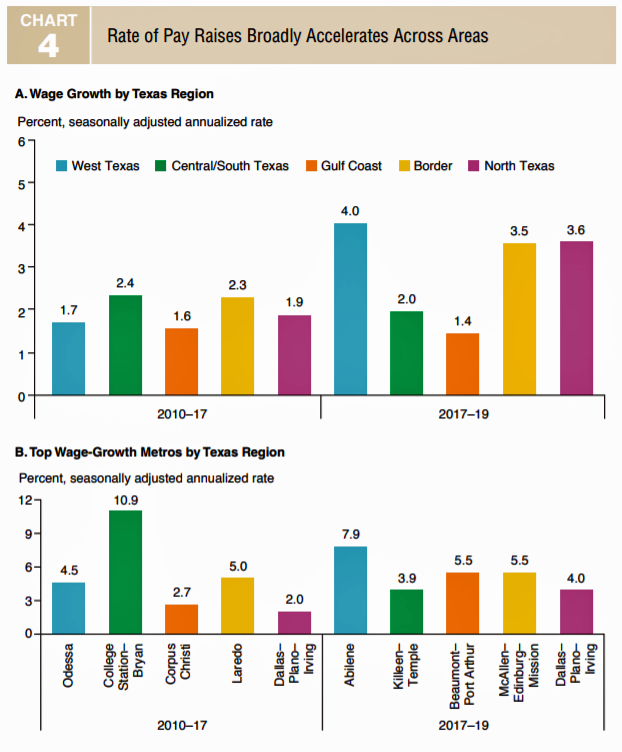

Wage growth by region has varied due to, among other factors, industry compositional differences and the lagged effects of labor constraints. However, most regions of the state have reported significant acceleration of average hourly wages since 2017 (Chart 4). In Texas and the U.S., wage growth from 2010 to 2017 was 2.0 per cent and 2.1 percent, respectively, but has since accelerated.

Within the state, some metros experienced particularly large increases. While wage growth was highest mostly in areas tied to energy from 2010 to 2017, it has since been strongest in mostly smaller metro areas with very low unemployment and weak labor force growth.

Wages in Abilene, which has a record-low 2.8 percent unemployment rate, rose by nearly 8 percent annually from 2017 through April 2019. Similarly, wage growth in McAllen–Edinburg– Mission, which has a record-low 5.4 percent unemployment rate, reached 5.5 percent over the period.

Across all industries, businesses are having difficulty finding any workers, skilled or unskilled, to expand. Wage growth may at some point encourage workers on the sidelines to reenter the workforce. Additional migration into Texas, whether domestic or international, could also alleviate worker shortages.

However, federal curbs on international migration and an improved national economy limit Texas’ ability to attract new workers.

Until the issue of shortages in Texas is resolved, it is likely that businesses will struggle trying to hire employees or replace workers lost in the course of normal turnover.

Job growth in the state over the past two years has held above the long-term average of 2 percent, and current estimates of 2019 growth suggest that this will continue, potentially sending the state unemployment rate even lower by year-end.

Christopher Slijk is an assistant economist in the Research Department at the Federal Reserve Bank of Dallas.

Notes

1 “New Technology Boosts Texas Firms’ Output, Alters Worker Mix,” by Emily Kerr, Pia Orrenius and Christopher Slijk, Federal Reserve Bank of Dallas Southwest Economy, Third Quarter, 2018, www.dallasfed.org/~/media/documents/research/swe/2018/swe1803b.pdf.

2 “Gone to Texas: Migration Vital to Growth in the Lone Star State,” by Pia Orrenius, Stephanie Gullo and Alexander T. Abraham, Federal Reserve Bank of Dallas Southwest Economy, First Quarter, 2018, www.dallasfed.org/~/media/documents/research/swe/2018/swe1801b.pdf

3 “Why Are Labor Markets for Blue-Collar Workers Tighter than for White-Collar Ones?” by Gad Levanon and Frank Steemers, Conference Board, Oct. 16, 2018, www.conference-board.org/blog/postdetail. cfm?post=6894.

4 See the Texas Business Outlook Surveys special questions, Nov. 26, 2018, www.dallasfed.org/research/surveys/tbos/2018/1811q.aspx.

Source: Federal Reserve Bank of Dallas