By Donald Hays

The median “wealth” or financial assets of U.S. households that participated in one or more means-tested government programs in 2017 was about 97% less than that of those who didn’t.

Despite less wealth and lower asset ownership, households that received government assistance surprisingly had only slightly lower unsecured debt, such as credit cards and medical bills, than those who didn’t and even lower secured debt like a mortgage.

The Survey of Income and Program Participation (SIPP) is the nation’s premier source of information on the characteristics of those who receive government assistance. The 2017 SIPP data show the disparities in levels of wealth and debt – the value of assets owned minus the liabilities (debts).

The U.S. Census Bureau report and detailed tables on household wealth in 2017 show wide variations across demographic and socio-economic groups.

One of these groups includes recipients of government programs such as Supplemental Nutrition Assistance Program (SNAP, previously known as food stamps); Medicaid; Supplemental Security Income (SSI); Special Supplemental Nutrition Program for Women, Infants, and Children (WIC); Temporary Assistance for Needy Families (TANF); and General Assistance (GA).

Households can participate in multiple programs at a time. Eligibility criteria for these government programs vary but are generally tied to income and sometimes include asset limits.

Here’s a deeper look at wealth and debt holdings of program participants, both overall and by program.

The overall financial picture of households that did not participate in any of the six government programs listed above is markedly different from those that did.

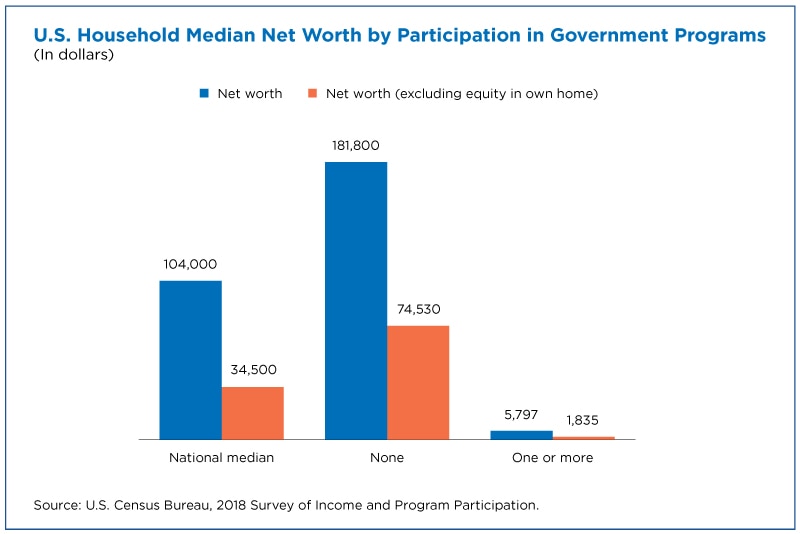

The median net worth, including home equity, of nonparticipants, was $181,800 — about 31 times more than the $5,797 of households that reported participating in one or more of these programs.

This wealth gap cannot be explained solely by the low rates of homeownership among program participants. The reason: Even when excluding home equity, program participants had less wealth ($1,835) than nonparticipants ($74,530).

Only 11% of nonparticipating households had a zero or negative net worth compared with 30% for participating households. In addition, only 39% of nonparticipating households had a net worth of less than $100,000 while 78% of participants were below that threshold.

WIC recipients were a particularly vulnerable group. WIC only benefits pregnant women, mothers of infants, infants, and children under five. Eligibility is benchmarked to income and a participant’s nutritional risk.

The assets and wealth of WIC recipients were substantially lower: a median net worth of only $3,244, which is 32 times less than the national median. In contrast, households where the youngest child was under 5 years of age (regardless of any program participation) had a median net worth of $38,420.

About 54% of WIC recipient households had a net worth below $5,000 and 36% had a zero or negative net worth. Their median checking account balance was only $500.

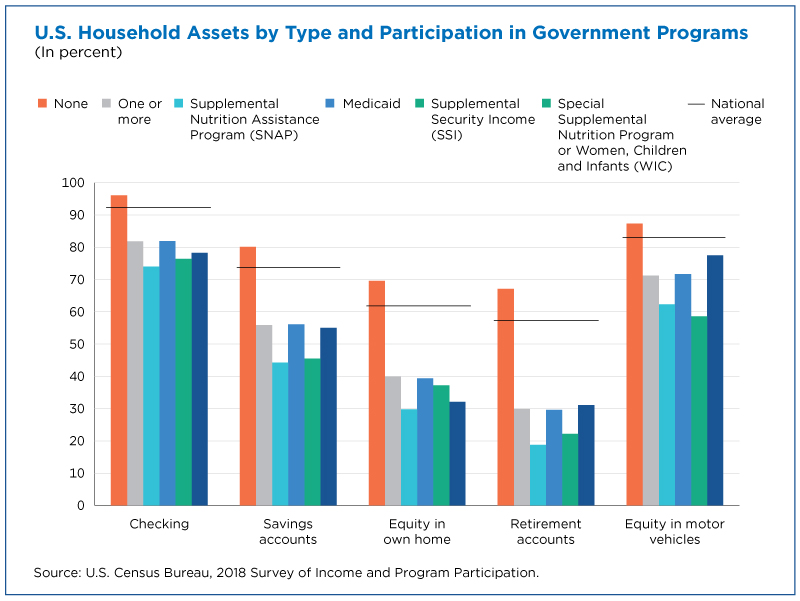

Households that participated in one or more government programs also had lower rates of asset ownership than those that did not receive assistance.

Here are ownership rates of the five most commonly held assets for program participants and nonparticipants:

Program participants not only had lower levels of asset ownership but the value of the assets was much lower.

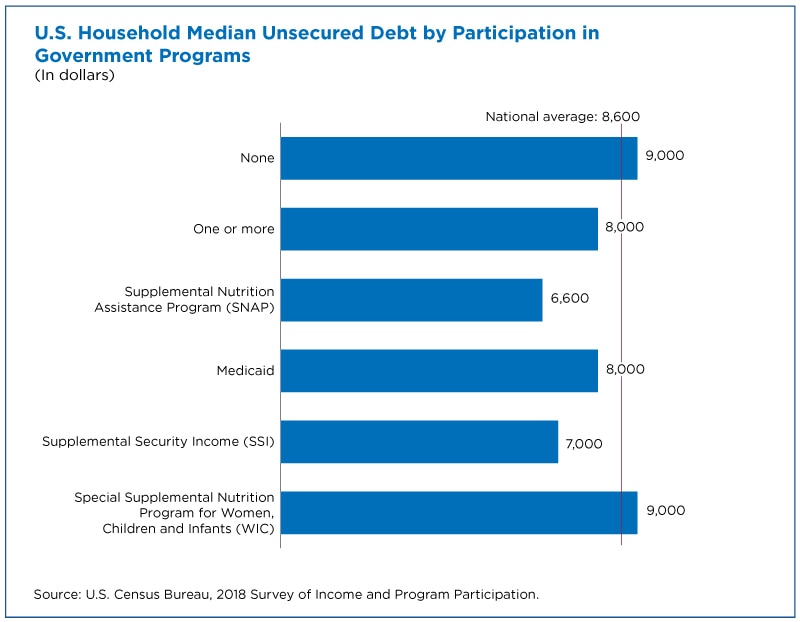

Despite lower measures of wealth and asset ownership among program participants, their levels of unsecured debt surprisingly were only slightly lower than of those who didn’t receive government assistance.

Sixty percent of those who did not participate in government programs had unsecured debt with a median value of $9,000. Among those who participated in one or more of these government programs, the percentage was slightly higher at 62% while the median value was lower at $8,000.

Those receiving government assistance were more likely to have medical debt but had slightly lower rates of credit card debt. Rates of student loan debt were equal between those with and without government benefits (22%) and the median student debt value was lower among participants.

Secured debt levels — “secured” by an asset such as a home or vehicle — of program participants were lower.

That suggests that those who, despite their lower asset levels, were able to buy a home or a car might buy older or more modest options which results in lower debt and asset values.

Donald Hays is a survey statistician in the Census Bureau’s Social, Economic, and Housing Statistics Division.

The San Marcos City Council received a presentation on the Sidewalk Maintenance and Gap Infill…

The San Marcos River Rollers have skated through obstacles after taking a two-year break during…

San Marcos Corridor News has been reporting on the incredible communities in the Hays County…

Visitors won't be able to swim in the crystal clear waters of the Jacobs Well Natural…

Looking to adopt or foster animals from the local shelter? Here are the San Marcos…

The Lone Star State leads the nation in labor-related accidents and especially workplace deaths and…

This website uses cookies.