Texas State Government And Long-Term Obligations Part Two – State Employee Pension Funding

![]() When a pension plan’s obligations exceed its assets, it is considered to have an unfunded liability. Unfunded pension liabilities have become a major concern for state and local governments across the U.S.

When a pension plan’s obligations exceed its assets, it is considered to have an unfunded liability. Unfunded pension liabilities have become a major concern for state and local governments across the U.S.

![]()

Over the next several days we will be running a special series from the Texas State Comptroller, Glen Hegar on the four issues below.

Part Two

Texas Comptroller Glenn Hegar today released a special edition of Fiscal Notes highlighting long-term financial obligations facing Texas state government.

Prior to the 2017 legislative session, Hegar sent a letter to lawmakers outlining some of these obligations which, if left unaddressed, could negatively impact the state’s credit rating and limit the amount of revenue available for general spending.

The report examines four of these obligations:

- state employee pension funding;

- the TRS-Care program, which provides health care coverage for retired public school employees and their dependents;

- the Texas Guaranteed Tuition Plan; and

- deferred maintenance projects for state buildings.

Texas State Government and Long-Term Obligations — Part Two

State Employee Pension Funding

Texas’ state and local government pension funds have more than 2 million members in 93 different plans.

The Employees Retirement System (ERS) manages three funds for different groups of public employees: ERS for most state employees; the Law Enforcement and Custodial Officers Supplemental Retirement Fund (LECOS); and the Judicial Retirement System Plan Two (JRS II).

The main ERS fund includes most state employees and all LECOS members, serving more than 185,000 active participants in all.1

Like most states, ERS still offers defined benefit plans (DBPs), which guarantee specific amounts of monthly income upon retirement.

Although both state agencies and their employees contribute to the pension fund, the investment risk is with the state as plan provider. (With defined contribution plans such as 401ks, by contrast, employers generally contribute a specific amount to employee retirement but have no further obligation to manage the funds.)

In 2016, 85 percent of all U.S. state and local government employees had access to a DBP, and 88 percent of those employees participated.2

When a pension plan’s obligations exceed its assets, it is considered to have an unfunded liability. Unfunded pension liabilities have become a major concern for state and local governments across the U.S.

In the Great Recession, many government pension systems’ unfunded actuarial accrued liability (UAAL) — the amount needed to meet all their future obligations — rose dramatically due to lower investment returns or even losses.

Consequently, dozens of government entities saw their credit ratings fall due to rising UAALs, including Dallas, Houston and the state of Illinois; the cities of Stockton, California, and Detroit, Michigan, declared bankruptcy due in part to unmet pension obligations.

While the obligations of Dallas and Houston won’t affect Texas’ state government balance sheet, both the Moody’s and Standard & Poor’s (S&P) rating agencies have warned Texas its credit rating could be in jeopardy if the state’s own pension liability isn’t addressed adequately.3

ERS doesn’t meet certain pension standards, but Texas still receives AAA-stable ratings. These ratings reflect expectations that the state’s leadership will:

- maintain budget and cash management discipline;

- address potential future budget gaps in a timely manner; and

- maintain sustainable UAAL levels by making the necessary contributions.4

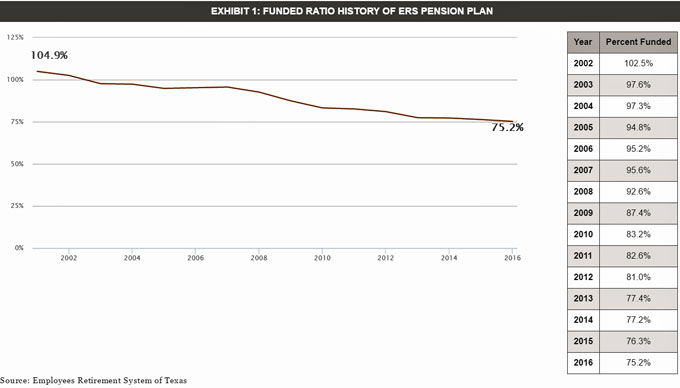

A pension plan’s average funded ratio — the ratio of its assets to its liabilities — is one measure of a plan’s health. Traditionally, a pension fund was considered “sound” at 80 percent or more, but other factors such as the size of the fund’s obligation and its funding policies and investment strategy all matter as well.5 As of August 2016, ERS had a funded ratio of 75.2 percent, down from 76.3 percent a year before (Exhibit 1).6

![]()

Challenges Facing ERS

Several factors are making the ERS pension fund’s viability uncertain, including:

- unrealistic assumptions about investment returns.

ERS assumes an 8.0 percent annual investment return but saw a gain of less than 0.5 percent in fiscal 2015 and 5.3 percent in fiscal 2016.7

This is a common problem; the national average assumed return for state pension programs was 7.5 percent in fiscal 2016, while the median actual return was 0.52 percent.8

Averaging good and bad years over time shows ERS’ average compound return was 7.7 percent during the last five years, 5.8 percent for the last 10 years and 7.4 percent for the last 25 years.9

These averages give a more accurate picture of ERS performance over time, but note that none meet the 8 percent assumption.

- inadequate contributions.

Texas Government Code §815.403 requires the state to make annual contributions to the ERS pension fund equal to 7.4 percent of the total compensation received by all ERS members in that year. Yet the state failed to meet this requirement in all but two years from 1988 through 2013.10 By one estimate, this cost the ERS pension fund more than $1.1 billion in contributions between 1991 and 2011 alone.11

The state also generally fails to make actuarially sound contributions (ASC) — that is, the level of contributions needed to fund the cost of future benefits and amortize (or gradually eliminate) the UAAL over a finite period.12 Texas’ contributions to the ERS fund have fallen below the ASC level each year since 2004.13

- demographic pressures.

Longer life expectancies are increasing fiscal pressure on pension systems. The average U.S. life expectancy was 69.7 in 1960 and 78.7 in 2010.14

- fewer contributing members.

In 2013, the ERS fund had 27 percent fewer contributing state employees than in 1995. A smaller contributor pool also affects returns on investment.

- early retirements.

Law enforcement and custodial officers, who represent 30 percent of the ERS population, are allowed to retire earlier, leaving fewer contributions and more lifespan to draw benefits.15

Prior Legislation

Since 2009, several state laws have attempted to address the ERS pension fund’s rising UAAL by increasing employee contributions, raising the retirement age and making other adjustments (Exhibit 2).16 S&P called changes made in 2015 in particular a “meaningful step toward constraining the future liability.”17

EXHIBIT 2: SIGNIFICANT LEGISLATIVE ACTIONS FOR ERS PENSIONS, 2009-2015

| Action | Affected Employees |

|---|---|

| Employee contributions increased by 0.5 percent to 6.5 percent | All employees |

| Eligibility for retirement annuity rules changed from 60 years old with five years of service to 65 with 10 years of service, or five years of service if the employee meets the Rule of 80 | Employees hired on or after Sept. 1, 2009 |

| Final average salary (FAS) increased from the average of the prior three years to four years | Employees hired on or after Sept. 1, 2009 |

![]()

| Action | Affected Employees |

|---|---|

| FAS increased to the average of the prior five years | Employees hired on or after Sept. 1, 2013 |

| Healthcare insurance premium contribution now based on years of service | Employees with less than five years of service credit on or before Sept. 1, 2014 |

| Unused sick and vacation leave can no longer be used to meet retirement eligibility | Employees hired on or after Sept. 1, 2013 |

| Employees who retire before age 62 have their annuity reduced by 5 percent annually for each year below that age | Employees hired on or after Sept. 1, 2013 |

| Employer contribution increased to 7.5 percent starting in fiscal 2014 | N/A |

| Each state agency to make a 0.5 percent contribution | N/A |

| Employee contributions to increase in increments from 6.5 percent to 7.5 percent by 2017 | All employees |

![]()

| Action | Affected Employees |

|---|---|

| State and member contributions both increased to 9.5 percent starting in fiscal 2016 | All employees |

| Employees given a 2.5 percent across-the-board pay raise to offset member contribution increase from 6.9 percent to 9.5 percent | All employees |

| 90-day membership waiting period for new hires eliminated | Employees hired on or after Sept. 1, 2015 |

Source: Employees Retirement System of Texas; Texas Department of Criminal Justice; Texas House of Representatives; and Texas Legislature online

Policy Options

Any change to government pension plans can involve significant challenges and may have unforeseen consequences. Before pursuing any significant change, a cost-benefit analysis should be conducted to fully understand how Texas’ pension funds and contributions would be affected.

Proposed policy options to improve the ERS pension fund’s finances include:

- raising member and/or state contributions.

Increasing member contributions would improve the fund’s financial health, but wouldn’t be popular with enrollees. ERS member rates are already above the national average, at 9.5 percent versus 6 percent. State rates are below the national average, at 10 percent versus 11.5 percent, but Article 16, Sec. 67(b)(3) of the Texas Constitution caps the state contribution at 10 percent.18 A constitutional change would be necessary unless the governor, following the constitutional provision, declares an emergency, in which case “the legislature may appropriate such additional sums as are actuarially determined to be required to fund benefits authorized by law.” Thus, increasing the state’s contribution would require the governor to declare an emergency or the Texas Constitution to be amended.

- making a one-time payment to the pension fund from general revenue or the Economic Stabilization Fund.

In the absence of further plan changes or major economic disruption, a payment of $1 billion would reduce the plan’s total obligations by $8.3 billion and fully fund it by 2041. A $4 billion payment would reduce obligations by $17.5 billion and fully fund the plan by 2028.19 A one-time payment would allow the funds to be invested at higher returns, lessen the need for changes to plan design and benefit structures and decrease the UAAL — but it wouldn’t prevent the UAAL from rising again in subsequent years if the state doesn’t meet the ASC.20

- selling pension obligation bonds.

In 2015, Kansas issued general obligation (GO) bonds to defray the cost of its employee pension systems, while bills supporting similar moves failed in Kentucky and Colorado. While this can be a viable option when interest rates are low, increased market exposure and required repayment schedules can make them risky.21 For this reason, the Government Finance Officers Association does not recommend the use of pension bonds.22

- reducing benefits offered to current and/or future hires.

This broad category of options includes increasing the retirement age; raising the number of years worked to become eligible for a pension; or reducing the multiplier that determines the size of the annuity.

Such options could reduce the UAAL over time, but reducing plan benefits is always controversial and can spur legal challenges, as seen recently in Rhode Island, where a benefit reduction led to several years of mediation and litigation.23

In addition, significant benefit changes could cause high-performing workers to seek employment elsewhere, reducing the overall quality of the workforce, or cause a “rush to retirement” among those at or near retirement age, reducing contributions and damaging the plan’s solvency.24

- changing the plan to a defined contribution or hybrid plan.

Supporters of defined contribution plans (DCPs) say they can give retirees more at retirement, and point to problems with DBPs such as higher costs, lack of personal control over investments, difficulties in transferring the plan to other employers and other inherent characteristics, such as the employer’s responsibility to maintain required fund balances regardless of market performance.25

Some research suggests otherwise, however. The state governments of Minnesota, California and New York each considered switching to DCPs and found that DBPs can cost less and achieve higher returns.26

Hybrid plans typically include mandatory contributions to both a DBP and a DCP, distributing the risk between employee and employer. The DBP portion provides a guaranteed monthly annuity while the DCP portion gives employees some control over their investment portfolios.

Because DCP contributions are invested separately from those for the DBP, employees may forego some earnings, since DBP pools focus on long-term assets that may yield higher returns over time. DCPs, therefore, need more funds to achieve the same level of benefit as a DBP.27

Hybrids, moreover, allow employees to leave their employer and take the DCP contributions with them, unlike DBP investments. Critics say this incentivizes employees to leave instead of staying for the long-term benefits offered by DBPs.

Endnotes

- Employees Retirement System of Texas, 2016 Comprehensive Annual Financial Report (Austin, Texas, December 2016), p. 3, available at https://www.ers.state.tx.us/About_ERS/Reports/. 146,390 active members of ERS and 39,066 active members of LECOS total 185,456 active members.

- U.S. Department of Labor, Bureau of Labor Statistics, “National Compensation Survey: Employee Benefits Survey,” https://www.bls.gov/ncs/ebs/benefits/2016/ownership/govt/table02a.htm.

- Moody’s Investors Service, “Moody’s: US States’ FY 2015 Net Pension Liabilities Reach $1.25 Trillion, with More Growth to Come,” October 6, 2016, https://www.moodys.com/research/Moodys-US-states-FY-2015-net-pension-liabilities-reach-125–PR_356175; and Standard & Poor’s Financial Services LLC, “Global Ratings, Summary: Texas; General Obligation; General Obligation Equivalent Security; Joint Criteria,” Dallas, Texas, October 2016, p. 5.

- Standard & Poor’s Financial Services LLC, “Global Ratings, Summary: Texas; General Obligation; General Obligation Equivalent Security; Joint Criteria,” p. 5.

- See for instance American Academy of Actuaries, “Issue Brief: The 80% Pension Funding Standard Myth,” July 2012, http://actuary.org/files/80%25_Funding_IB_FINAL071912.pdf.

- Employees Retirement System of Texas, Actuarial Valuation Reports for Pension Plans Administered by ERS as of August 31, 2016, by Gabriel Roeder Smith & Company (Austin, Texas, August 2016), p. 12, available at https://www.ers.state.tx.us/About_ERS/Reports/.

- Standard & Poor’s Financial Services LLC, “Global Ratings, Summary: Texas; General Obligation; General Obligation Equivalent Security; Joint Criteria,” p. 4.

- Moody’s Investors Service, “Moody’s: US States’ FY 2015 Net Pension Liabilities Reach $1.25 Trillion, with More Growth to Come.”

- Employees Retirement System of Texas, Actuarial Valuation Reports for Pension Plans Administered by ERS as of August 31, 2016, p. 10.

- Texas State Employees Union, “A Pension Primer for State Employees,” p. 5, http://www.cwa-tseu.org/wp-content/uploads/2013/01/2014_2015-State-Employee-Pension-Primer.pdf.

- Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature (Austin, Texas, September 4, 2012), p. 29, www.ers.state.tx.us/About-ERS/Reports/IBS-Retirement/.

- Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature, p. 28.

- Employees Retirement System of Texas, Actuarial Valuation Reports for Pension Plans Administered by ERS as of August 31, 2016, p. 17; and Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature, p. 61.

- National Center for Health Statistics, “United States Life Tables, 2011,” by Elizabeth Arias, National Vital Statistics Reports (Hyattsville, Maryland, 2015), vol. 64, no. 11, September 22, 2015, p. 45, https://www.cdc.gov/nchs/data/nvsr/nvsr64/nvsr64_11.pdf.

- Employees Retirement System of Texas, “Issue Brief: ERS and TRS,” p. 1, available at https://www.ers.state.tx.us/About_ERS/Reports/Overview/.

- Sources for Figure 2 include Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature, p. 6; Texas Department of Criminal Justice, “Summary of Retirement Changes included in SB 1459,”

https://www.tdcj.state.tx.us/documents/announcements/Proposed_Retirement_Legislation_SB1459_Update_05-21-13.pdf; and Texas House of Representatives, Committee on Appropriations, Subcommittee on Articles I, IV, & V (Austin, Texas, April 2016), pp. 4-7, http://www.legis.state.tx.us/tlodocs/84R/handouts/C0132016042010001/1ea1be52-2f44-4a96-acd9-b97f327bd483.PDF. - Standard & Poor’s Financial Services LLC,“Global Ratings, Summary: Texas; General Obligation; General Obligation Equivalent Security; Joint Criteria,” pp. 4-5.

- Texas House of Representatives, Committee on Appropriations, Subcommittee on Articles I, IV, & V, p. 43; and Tex. Const. Article 16, §67.

- Texas House of Representatives, Committee on Appropriations, Subcommittee on Articles I, IV, & V, p. 23.

- Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature, pp. 31-32.

- Sarah Breitenbach, “Despite Risks, State and Local Governments Turn to Pension Obligation Bonds,” Stateline (August 12, 2015), http://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2015/08/12/despite-risks-state-and-local-governments-turn-to-pension-obligation-bonds.

- Government Finance Officers Association, “Pension Obligation Bonds,” http://www.gfoa.org/pension-obligation-bonds.

- Katharine Q. Seelye, “Rhode Island Settles Lawsuit on Union Pension Overhaul,” New York Times (April 2, 2015), https://www.nytimes.com/2015/04/03/us/rhode-island-settles-lawsuit-on-union-pension-overhaul.html?_r=0.

- Brookings Institution, Financing State and Local Pension Obligations: Issues and Options, by William G. Gale and Aaron Krupkin, July 2016, p. 2, https://www.brookings.edu/wp-content/uploads/2016/07/PB-Pension-shortfalls-and-SL-budgets.pdf; and Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature, pp. 33-34.

- Texas Public Policy Foundation, Reforming Texas’ State & Local Pension Systems for the 21st Century, by Arduin, Laffer & Moore Econometrics, April 2011, pp. 6-15, http://www.texaspolicy.com/library/doclib/2011-04-RR05-ReformingTexasStateLocalPensionSystems-laffer.pdf.

- Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature, pp. 47-49, 56.

- Employees Retirement System of Texas, Sustainability of the State of Texas Retirement Program: Report to the 82nd Texas Legislature, p. 53.

This series was originally published by the Texas State Comptroller, Glen Hegar.