Motor Fuels Taxes In A Changing Texas Transportation Scene

Since 1923, Texas has used revenue from its motor fuels excise taxes to build and maintain our state highways, roads and bridges. In a century, our population — and our traffic — have soared.

Automobiles have become much more fuel efficient and, increasingly, are being joined on our roads by hybrid and fully electric vehicles. But while driving has changed drastically, the taxes we depend on to fund our road infrastructure haven’t.

TEXAS MOTOR FUELS TAXES

In fiscal 2018, Texas motor fuels taxes brought in $3.7 billion, about 6.6 percent of all state tax collections. In that year, they were the state’s fourth-largest source of tax revenue after the sales tax, the motor vehicle sales and rental tax and the franchise tax.

The majority of our motor fuels tax revenue is used for transportation projects. In Texas, gasoline and diesel fuel are subject to a 20-cent tax per gallon. In addition, the federal government imposes taxes of 18.4 cents per gallon on gasoline and 24.4 cents per gallon on diesel fuel.

According to the American Petroleum Institute, when taking into account the federal tax (and other applicable state taxes and fees, although Texas has none of these), Texas’ total levies on gasoline and diesel are the nation’s seventh-lowest and fourth-lowest, respectively, and by far the lowest among the 10 most populous states. Texas drivers pay total levies of 38.4 cents per gallon on gasoline, versus nearly 74 cents in California and 60.4 cents in Florida, for example.

Texas’ gasoline and diesel tax rates haven’t changed since 1991, while the federal rates were last changed in 1993. In the years since, fuel prices have tripled — but since the taxes are based on volume rather than price, tax collections have risen much more slowly.

ROUGH ROADS AHEAD?

The Texas Department of Transportation’s (TxDOT) Texas Transportation Plan 2040 identifies several major challenges facing the state, including an aging transportation infrastructure, inflation, greater fuel efficiency and shaky funding from a federal Highway Trust Fund it describes as “near insolvency.” Today, Texas’ motor fuels taxes are simply failing to produce the revenue needed to meet these challenges.

Since 1990, Texas’ population has risen by 55 percent while Texans’ average daily vehicle miles traveled have increased by 70 percent. TxDOT’s transportation plan estimates the state’s population will rise to 45 million by 2040, putting further strains on an already overburdened road infrastructure.

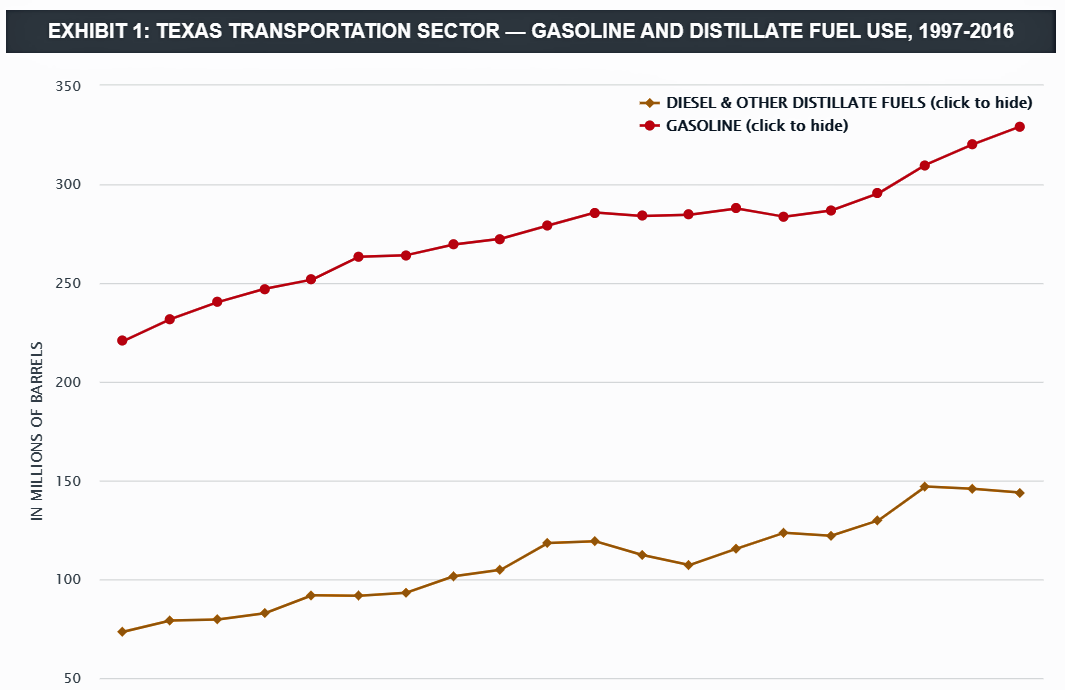

According to the U.S. Energy Information Administration, the amount of gasoline used annually by Texas’ entire transportation sector (including rail, air and marine uses as well as autos) rose by 49 percent between 1997 and 2016, to 329 million barrels (Exhibit 1).

Its use of diesel and other distillate fuels rose by 96 percent in the same period. Texas’ annual growth rate for gasoline consumption has surpassed that of the nation as a whole in every year since 2005.

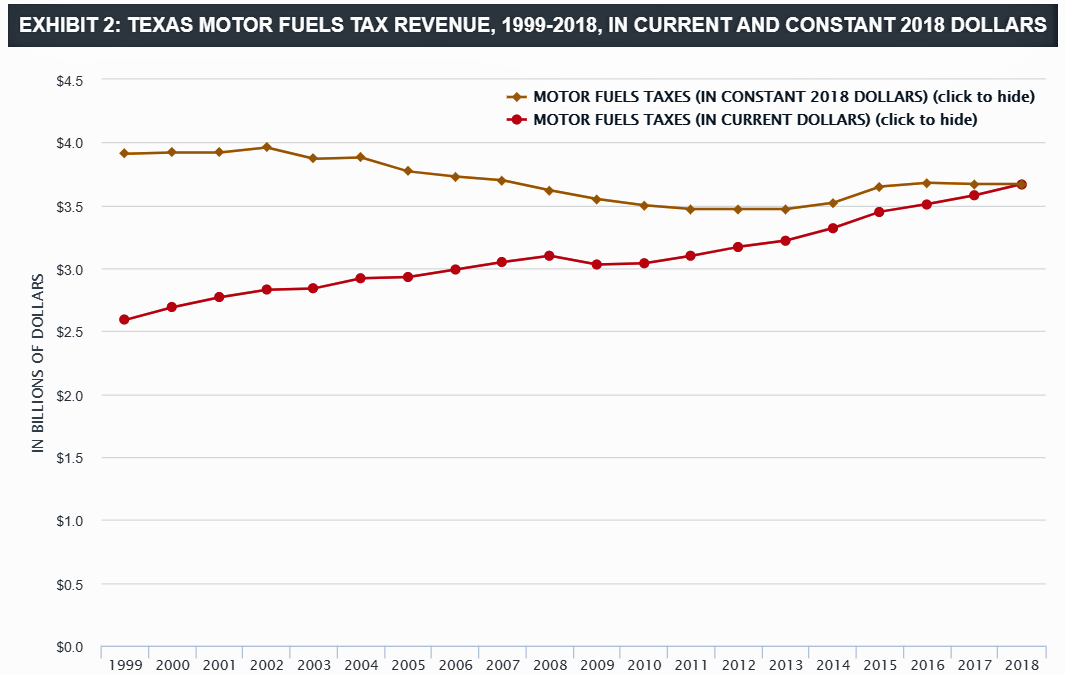

After adjusting for inflation, however, Texas’ motor fuels tax revenue has actually declined during the last two decades (Exhibit 2).

Experts at the Texas A&M Transportation Institute (TTI) have suggested that Texas’ motor fuel revenue is likely to peak around 2030 and then begin to fall, thanks to increasing fuel efficiency and an apparent leveling off of per-capita vehicle miles traveled.

Since 1978, the fuel economy of American cars and light trucks has been governed by the National Highway Traffic Safety Administration’s Corporate Average Fuel Economy (CAFE) standards.

Over time, CAFE standards have gradually increased; the current rule would require automakers to have an average fuel economy of 54.5 miles per gallon by model year 2025.

While Congressional attempts are under way to freeze those increases, fuel efficiency is likely to continue improving — meaning less motor fuel use and less tax revenue per mile.

Alternative-fuel vehicles — hybrids, all-electric cars and trucks and those fueled by natural gas and propane — will have a growing impact. While the number of alternative-fuel vehicles has risen by about 10 percent annually over the last few years, they made up only 1 percent of the 24.6 million registered vehicles on Texas roads in fiscal 2018.

Even so, TTI predicts that these vehicles will account for 18 percent of U.S. domestic cars and trucks and 11 percent of commercial vehicles by 2040 — and that increasing use of alternative fuels could reduce annual state revenue by almost $200 million by 2035.

EXHIBIT 1

TEXAS TRANSPORTATION SECTOR — GASOLINE AND DISTILLATE FUEL USE, 1997-2016

EXHIBIT 2

EXHIBIT 2

TEXAS MOTOR FUELS TAX REVENUE, 1999-2018, IN CURRENT AND CONSTANT 2018 DOLLARS

Sources: U.S. Bureau of Labor Statistics and Texas Comptroller of Public Accounts

Sources: U.S. Bureau of Labor Statistics and Texas Comptroller of Public Accounts

RISING ROAD COSTS

While motor fuels tax revenue is showing little growth and may even decline, the cost of maintaining our aging highways and roads — and building more — is rising dramatically.

The Federal Highway Administration’s National Highway Construction Cost Index, used by planners and policymakers to calculate the inflation of highway construction costs for items such as asphalt and machinery, has risen by 84 percent since 2003, far surpassing the general inflation rate of 33 percent during the same period.

According to 2016 testimony from the TTI, due to rapid inflation the 20-cent motor fuels tax “now purchases less than 10 cents’ worth of construction.”

While the challenge is particularly acute in Texas because of our rapid growth, it’s a nationwide problem. In fiscal 2013, according to the Tax Foundation, state-level gas taxes, tolls and license fees produced enough revenue to cover only 41.4 percent of state spending on roads.

At the federal level, the Congressional Budget Office has estimated the Highway Trust Fund may be insolvent as soon as 2021, while the National Surface Transportation Infrastructure Financing Commission projects a cumulative, nationwide highway investment funding shortfall of $2.3 trillion through 2035.

OTHER STATES LOOK FOR MONEY

Many states have recognized that existing motor fuels taxes can’t fully support rising needs and costs. In its 2016 testimony before the Texas House, TTI noted that 26 states were funding road construction projects with revenue bonds; 24 states were using general obligation bonds; and 33 had employed public-private partnerships.

In addition, many states have financed projects with tools such as tax increment financing or transportation reinvestment zones, both of which use property tax growth from a specific geographic zone to pay for improvements within it.

According to the National Conference of State Legislatures (NCSL), 31 states have raised their motor fuels tax rates since 2013, including four in 2019. But fuel tax hikes were rejected in Massachusetts in 2014 and Missouri in 2018, for instance.

A 2019 University of Texas/Texas Tribune poll found that 72 percent of Texas voters wouldn’t support a similar tax increase.

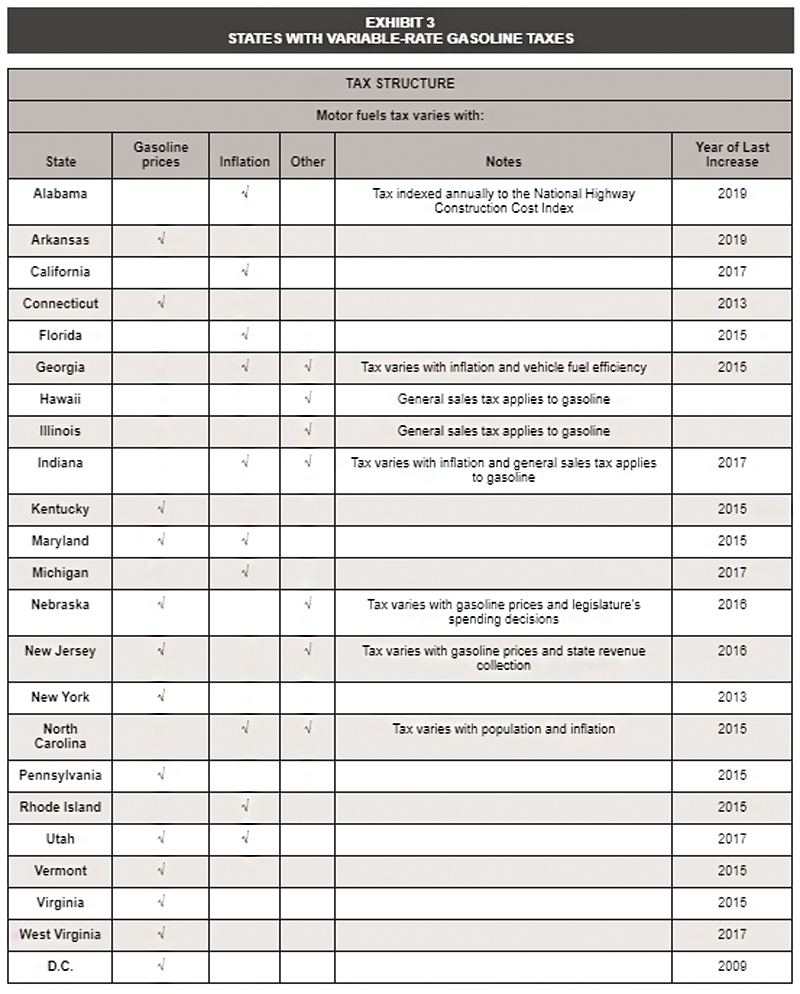

Many states have adopted variable-rate gas taxes. These tax rates are indexed to some external statistic such as the inflation rate or the price of gasoline, and can be used alone or in conjunction with a volume-based tax.

NCSL reports that 22 states and the District of Columbia have implemented some form of variable-rate gasoline tax (Exhibit 3).

EXHIBIT 3

STATES WITH VARIABLE-RATE GASOLINE TAXES

One type, used by several states, is a tax on the wholesale or “rack” price of gasoline. (The rack price is the price at which refineries sell gasoline to their various clients, including wholesalers or gas stations.)

While this generates more revenue when gas prices are high, it obviously leaves states vulnerable when prices fall. Since 2015, when oil prices fell sharply, Kentucky, North Carolina and California have found themselves forced to scramble for additional transportation revenue.

Nine states have linked the gasoline tax to the Consumer Price Index (CPI) or another inflation measure. Still others have tied the variable rate to metrics such as population or certain legislative appropriations.

Three states, Hawaii, Illinois and Indiana, apply their general sales tax to gasoline in addition to the motor fuels tax. And in 2015, Georgia linked its motor fuels tax to fuel efficiency standards as well as CPI.

Some states have begun rethinking the gasoline tax entirely, exploring funding methods tied more closely to actual use. Examples include greater use of toll lanes or mileage-based user fees, which have been piloted in several states.

The National Surface Transportation Infrastructure Financing Commission has called such measures “the consensus choice for the future.”

In 2015, Oregon became the first U.S. state to test a road usage charge program, called OReGO. Drivers opting in to the program agree to tracking with a mileage-reporting device and pay 1.5 cents per mile, while receiving a tax credit for the standard gasoline tax that is automatically applied to their road usage charges.

Despite privacy concerns, more than 1,300 Oregon vehicles are currently enrolled in the program.

NEW MONEY FOR TEXAS ROADS

In November 2014, Texas voters overwhelmingly passed Proposition 1, which directs more funding to the state’s transportation needs.

Prior to Prop 1, the state’s Economic Stabilization Fund (ESF), the “rainy day fund,” received 75 percent of the state’s annual oil and natural gas production tax revenue in excess of fiscal 1987 revenues.

Proposition 1 now allocates up to half of that revenue to the State Highway Fund (SHF) — $1.38 billion in fiscal 2019.

The allocations to the SHF will end after the fiscal 2035 transfer if the Legislature doesn’t renew them.

In 2015, voters approved Proposition 7, potentially the largest increase in transportation funding in Texas history.

This amendment directs the Comptroller’s office to deposit up to $2.5 billion of net revenue annually into the SHF from the state sales tax, after total sales tax receipts exceed $28 billion.

The deposits will cease in fiscal 2032 unless the Legislature extends the arrangement.

Beginning in fiscal 2020, Proposition 7 further directs the Comptroller’s office to annually transfer to the SHF 35 percent of state motor vehicle sales tax revenue above the first $5 billion collected. Without legislative action, this will expire in 2029.

Federal legislation has added to Texas transportation funding as well.

The 2015 Fixing America’s Surface Transportation Act (FAST) provides federal funding to state and local governments to assist with mobility needs. Under FAST, Texas is receiving $18.3 billion in additional highway funding for fiscal 2016 through fiscal 2020.

Yet even these additional funding streams won’t address the entire problem. As population and traffic congestion continue to grow, Texas policymakers may consider alternatives.

Source: Office of State of Texas Comptroller